portability estate tax exemption

Learn With CPA Self Study. After that the executor would have to file for a letter ruling and submit substantial evidence to extend the portability.

What Is Portability For Estate And Gift Tax Portability Of The Estate Tax Exemption The American College Of Trust And Estate Counsel

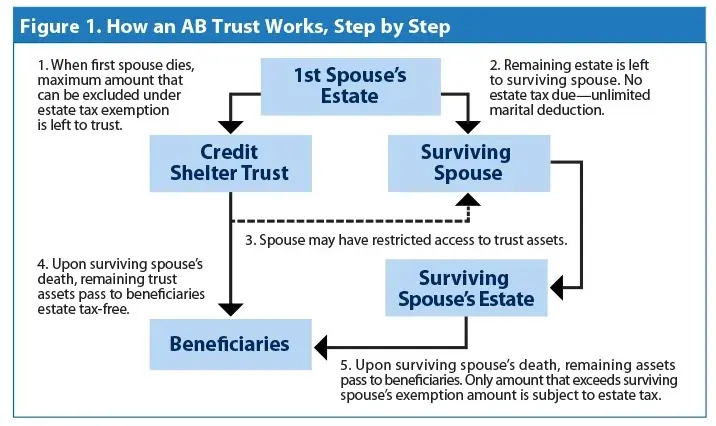

Prior to the enactment of the portability law in 2010 most estate plans for married couples set aside at the first.

. Attach a statement to the return that refers to the particular treaty applicable to the estate and write that the estate is claiming its benefits. Ad Practical And Affordable CPE Courses For CPAs. So if your spouse passed away less than five years ago you may be able to file an.

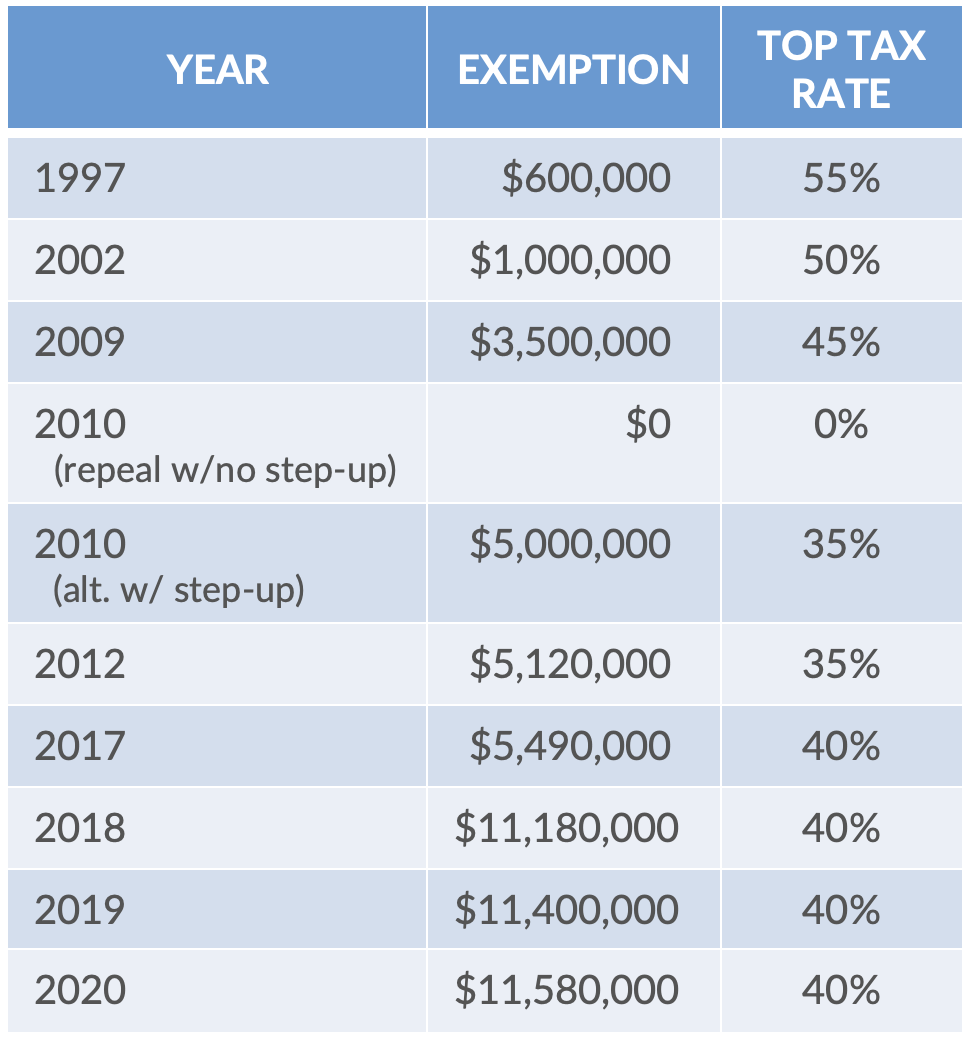

However that exemption is scheduled to return to 5000000 as adjusted for inflation in 2026. Understand the different types of trusts and what that means for your investments. Ensuring use of the first-to-dies exemption or capturing as much as possible based on the assets in his or her estate generally meant funding assets into a credit shelter trust for the surviving spouse.

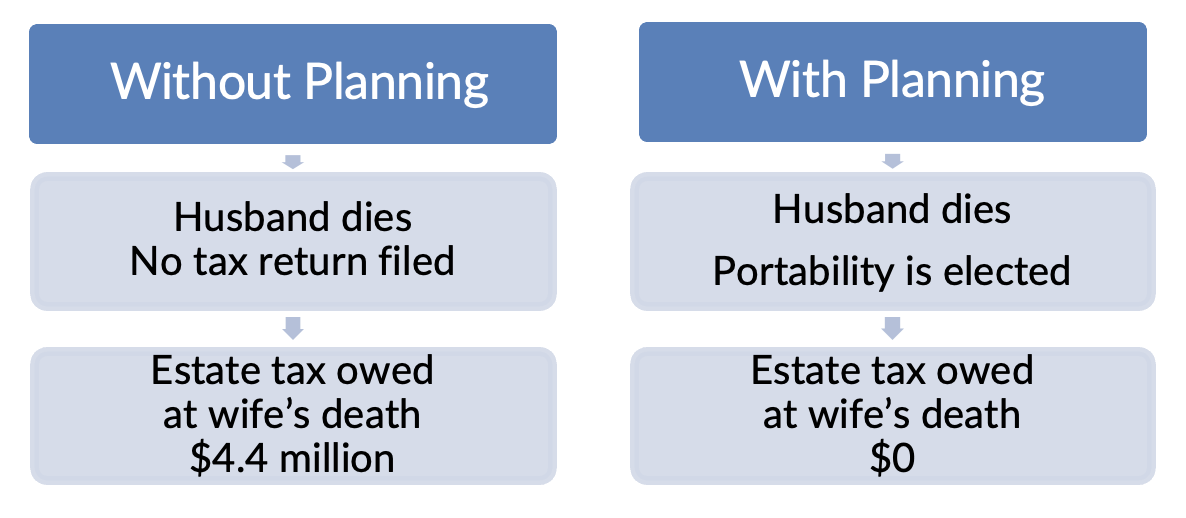

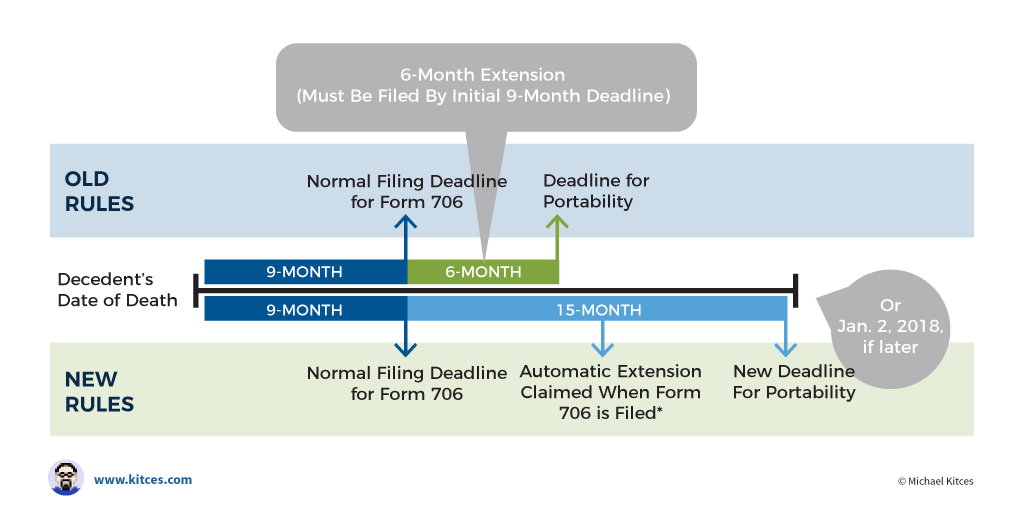

The wife has to file the IRS Form 706 federal estate tax returns to get the portability within 270 days after her husbands death. On July 8 2022 the Internal Revenue Service issued new guidance that allows a deceased persons estate to elect portability of their unused gift and estate tax exemption for up to five years after their death. There is not as much need to split the exclusions and have the estate of the first spouse to pass away get allocated into a credit shelter trust or bypass trust.

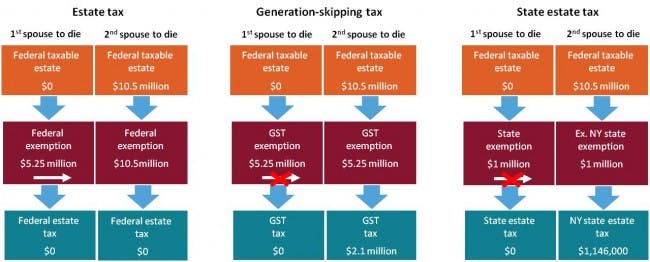

The federal estate tax exemption and gift exemption is presently 1206 million. The estate tax return is due within nine months of death and can be extended for another six months if the estate timely files an extension. Assets are exempt from US.

This post will discuss the general rules of portability. Thanks to the portability rule the survivor can use whats left. It allows the spouses to go about their estate planning and transfer assets upon their death the way that they would like to to carry out their wishes.

That gives the couple a total exemption of more than 234 million. The Tax Cuts and Jobs Act increased the federal estate tax exemption in 2018 and it has increased since then adjusting with inflation so its no surprise that the exemption is higher for 2022. To elect portability the estate of the first deceased spouse needs to file Form 706 United States Estate and Generation-Skipping Transfer Tax Return.

Prior to portability any unused estate tax exemption of the first spouse to die was simply lost. When a spouse dies the surviving spouse has the option of taking the unused federal estate tax exclusion and applying it to their own estate. It is twice the amount for married couples.

Electing to use estate tax portability makes a significant difference in your federal estate tax liability. Even if a deceased spouse did not have a taxable estate the couples combined estates could be very substantial. Portability also applies to gift tax and therefore the gift tax exemption is also 16880000 for the survivor.

Regarding the estate tax exemption for couples. And then after one spouses death then the surviving spouse can take steps to combine their estate tax exemptions to reduce estate tax. Please note that these exemption amounts are for individuals.

For decedents dying in 2011 and 2012 the personal representative can elect to transfer the deceased spouses unused exemption to his or her surviving spouse. If the portability election is filed in time the entire estate of 60 million will be named under the wife. Because the federal estate tax exemption is set to.

Entries for the gross estate in the US the taxable estate and the tax amounts should be 0 if all of the decedents US. With exemption levels being indexed for inflation the exemption amount has gone up still. By Natasha Meruelo.

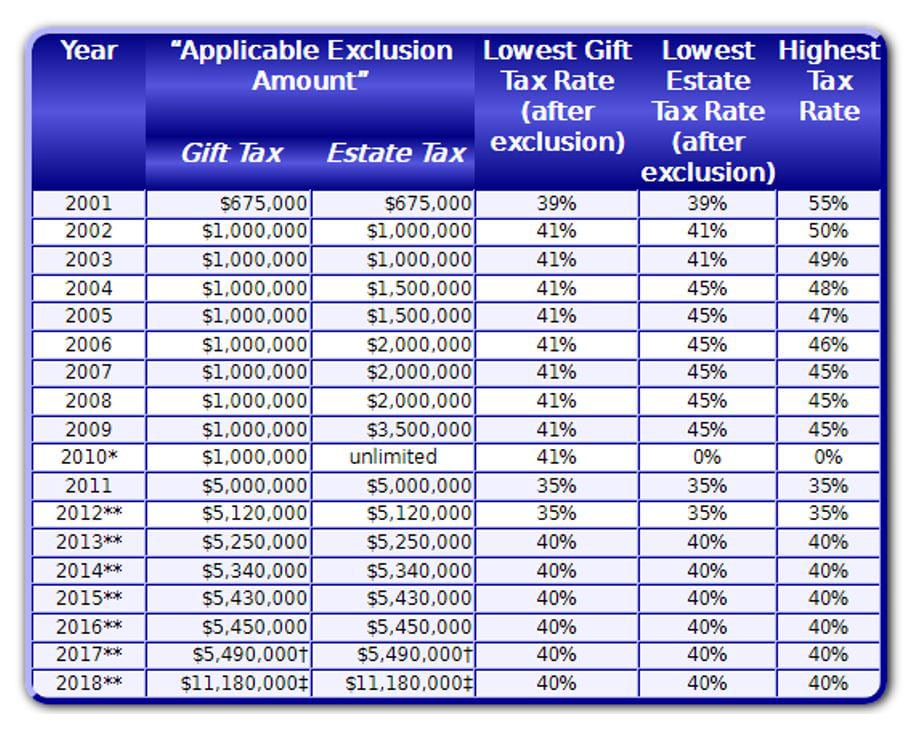

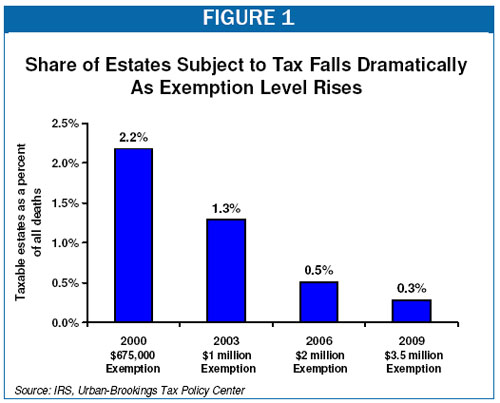

The estate and gift tax exemption was 1 million in 2002. Especially for couples with a joint. Please note these laws being permanent means that they are not set.

As of that time the estate tax exemption was much lower. The non-exempted amount of 545 million would be portable and would be passed to his wife. After all electing portability could mean that a surviving spouse could have double the estate tax exemption at the second death currently 5430000 x 2 10860000.

Portability allows a surviving spouse the ability to transfer the deceased spouses unused exemption amount DSUEA for estate and gifts taxes to a surviving spouse so long as the Portability election is made on a timely filed federal estate tax return IRS Form 706. 247 Access To More Than 130 Courses. If you elect Portability the assets will receive a basis step-up at.

Ad Take out the guesswork with The Investors Guide to Estate Planning for 500k portfolios. The key advantage of portability is flexibility. It sat at 114 million for 2019 1158 million for 2020 and it has now hit 117 million for 2021.

Therefore the objective should be to get the survivors estate at or below the 4000000 threshold for Illinois. This is known as taking Portability Exemption Relief for the DSUE Deceased Spousal Unused Exemption according to a recent article Estates can now request late portability election relief for 5 years. 7031 Koll Center Pkwy Pleasanton CA 94566.

This was just the estate tax portability rules though. Currently the federal estate tax exemption is 11400000 per spouse. The need for splitting the estate into.

Subscribe And Save More At CPA Self Study Online. As of January 1 2026 unless the law changes the federal estate tax exemption will fall to 6 million. The Illinois estate tax on an estate of 16880000 would be 1524400.

The estate and gift tax exemption is the amount you can transfer to individuals other than your spouse free of estate and gift taxes during your lifetime or at your death Generally speaking you can transfer as much as you want to your spouse without incurring estate and gift taxes. After 2012 one important question for estate planning is whether or not portability should be elected at the first death. Portabilitys Effect on Tax-Efficient Estate Tax Planning.

When the surviving spouse later dies or makes a lifetime gift the surviving spouse will have his or her own. If during hisher lifetime the survivor. Estate tax pursuant to the applicable treaty.

The federal Estate Tax commonly referred to as the death tax is a tax on a persons right to transfer property upon their death. Each year the government sets a tax exemption limit or exclusion amount for estates under a. A married couple can transfer 2412 million to their children or.

Portability essentially allows two spouses to combine their estate exclusions together into one large exemption. A surviving spouse can get a big federal estate tax break if the deceased spouse didnt use up his or her individual estate tax exemption. Effective July 8 2022 the IRS issued Revenue Procedure 2022-32 to supersede Revenue Procedure 2017-34 and now allow for a late estate tax exemption portability election to be made up to.

Locking In A Deceased Spouse S Unused Federal Estate Tax Exemption

What Surviving Spouses Need To Know About The Marital Portability Election Natural Bridges Financial Advisors

Portability Of A Spouse S Unused Exemption 1919ic

Portability Of A Spouse S Unused Exemption 1919ic

Historical Estate Tax Exemption Amounts And Tax Rates 2022

Is Ab Trust Planning Still Effective

Understanding Qualified Domestic Trusts And Portability

Tax Related Estate Planning Lee Kiefer Park

Irs Announces 2017 Estate And Gift Tax Limits The 11 Million Tax Break

Historical Estate Tax Exemption Amounts And Tax Rates 2022

Portability Of Unused Estate And Gift Tax Exclusion Between Spouses

Credit Shelter Trusts And Portability Eagle Claw Capital Management

Portability Enabled Traditional Trusts Clark Trevithick Full Service Boutique Law Firm In Los Angeles California Southern California

Portability Becomes Permanent Baker Tilly

Power Of Portability This Estate Tax Tool Can Save You Millions Agweb

Form 706 Extension For Portability Under Rev Proc 2017 34

Exploring The Estate Tax Part 2 Journal Of Accountancy

Estate Planning Can Secure Your Legacy Jackson Fox Pc Ardmore Ok

The State Of The Estate Tax As Of 2006 Center On Budget And Policy Priorities